Mastering Credit Management: Essential Strategies and Insights

The majority of the links on our website are affiliate links. This means that if you click on the link and make a purchase, we earn a small commission at no additional cost to you.

2

Step 1 is universal; you can’t go into the process blind. You need to know what is in your profile that the credit bureaus store about you. Only you are going to know if there are any errors in your credit file by reviewing your credit reports. Since creditors and lenders are not required to report to the credit bureaus.

And the credit bureaus only know what is reported to them, ordering your reports from them is important. You only want to address errors with the credit bureau that shows errors on their report of you. With the assumption that you ordered and now have your credit reports. Here are three things to do before you inform the credit bureau of any errors. Below are three actions you can do before you begin disputes.

Navigate Credit Offers Wisely

By staying informed about common financial practices and understanding marketing motivations, you can shield yourself from deceptive offers and make well-informed financial decisions. I thought receiving offers in the mail for credit cards was because I had good credit. Because credit card offers don’t come in the mail when your credit is bad. Although, these credit card offers do not guarantee that line of credit.

The credit bureaus are a storage house for your file. Containing information reported to them by your creditors. Your creditors own the information they are reporting. Credit bureaus assume the information is accurate. The credit bureaus also sell the information to other creditors, loan providers, insurance providers and mortgage companies.

Loan providers and credit card companies are aiming to offer credit to consumers. But not all consumers are going use credit responsibly. They want to find the consumers who pay their debts. Surprisingly credit scores are a great indicator for that. Creditors and lenders use software that analyze credit reports based on specific criteria.

Such as, targeting consumers with credit scores ranging from 600 to 680. Because they know consumers who fall into that range are more likely to accept higher interest rates compared to consumers with excellent credit scores. Or a creditor might want to target individuals who have high credit scores but are currently underserved by their existing credit cards.

You want the right amount and mix of credit to earn the most points whenever your credit score is calculated. In terms of credit cards, 3 earns the most points. But more importantly, being able to manage them well is what’s going to build a solid credit profile. If you feel ready to take on credit by applying for a loan or a credit card. You can easily search online for options. You don’t need mailing offers.

Shield Your Finances: How Opting Out at OptOutPrescreen.com Protects You From Identity Theft

Opting out helps to prevent credit card offers from falling into the wrong hands, as criminals could exploit them to steal your identity. Fraudsters could apply for credit in your name, accumulate debts without your awareness, leading to collections and ugly credit reports. You can opt-out at www.optoutprescreen.com

If you fall victim to identity theft, immediate action is necessary to minimize damage and safeguard yourself:

- File a Report: Contact your local police department to file an official report of the identity theft.

- Contact Credit Bureaus: Notify major credit bureaus—Experian, Equifax, and TransUnion—about the identity theft. Request a fraud alert on your credit report to prompt creditors to verify your identity before extending credit.

- Maintain Detailed Records: Keep thorough records of all communications, transactions, and documents related to the identity theft, including copies of correspondence and police reports.

- Seek Assistance: If unsure about the necessary steps, consider consulting a certified identity theft specialist or legal professional for guidance.

Take Control: How the Do Not Call Registry Reduces Unwanted Calls and Protects Your Privacy

The primary goal of the Do Not Call Registry is to give people a choice about whether they want to receive telemarketing calls at home. It was established to address consumer complaints about unwanted telemarketing calls and to provide a straightforward mechanism for stopping those calls.

This will not stop all solicitation calls altogether. Most telemarketing calls are covered by the registry. However, there are exceptions. Calls from political organizations, charities, telephone surveyors, or companies with whom a consumer has an existing business relationship are allowed. A company may call a consumer for up to 18 months after the consumer’s last purchase, delivery, or payment—even if the consumer’s number is on the registry.

But it will substantially reduce solicitation calls. While some automated systems and international scammers may ignore the registry as well, taking control of your financial matters shouldn’t entail wasting time on fake scare tactics, such as fraudulent calls claiming computer issues from supposed Microsoft representatives.

If you fall victim to a phone scam and provide your banking information to a criminal who proceeds to withdraw funds, your bank will not be liable for reimbursement. Never disclose sensitive information over the phone, especially if you didn’t initiate the call, as the identity of the caller cannot be guaranteed. Registration is quick and easy online, but it takes 31 days to take full effect. Afterward, if a solicitor violates your rights by calling, you have the right to demand compensation or pursue legal action through small claims court. www.DoNotCall.gov.

Lock Down Your Credit: The Essential Guide to Freezing and Unfreezing Your Credit Report

Don’t overlook the importance of freezing your credit reports. Place a freeze on your credit reports now; or if you are in the process of applying for a credit card to build positive credit, do it immediately afterward. Frozen credit reports means no one can open, read, or obtain your credit report. It is “frozen shut.” When applying for credit in the future, instruct the credit bureaus to unfreeze your report for a specific period, such as one week or one month.

If applying for a home loan, your credit reports need to be unfrozen and open to the mortgage lender from the initial application until the loan closes. For other types of credit, inquire about the necessary time period. Allow a couple of days for your unfreeze request to go through.

Experian states that when you execute the request to lift the freeze, it happens in an hour; however, it could take two days to go through. Remember, there’s an additional charge to request it again after lifting the freeze, so don’t overlook this.

Freezing your credit shields you from online identity theft, unauthorized credit usage, and unapproved credit inquiries. However, it doesn’t prevent you from accessing your own credit report, nor does it stop review by current creditors, collection agencies, or landlords.

If you have children, consider freezing their credit to safeguard them from fraud. Freezing their credit is the most effective prevention measure. If a child falls victim to credit fraud, report it to the authorities and provide a copy of the police report to both the creditor and credit bureaus to shut down the account and remove it from the child’s file.

You can easily freeze your credit online, or if preferred, you also have the option to submit a freeze request by mail or telephone. Below are the links for freezing your credit with major credit bureaus:

Experian: Link

Equifax: Link

TransUnion: Link

Innovis: Link

LexisNexis (joint with SageStream): Link

SageStream (joint with LexisNexis): Link

Clarity Services: Link

Once you’ve completed the freezing of your credit, it’s prudent to wait for a two-week period before sending any dispute or challenge letters. Keep in mind, this waiting interval is a critical aspect of the setup process, and exercising patience is paramount.

Beyond the Big Three: Exploring Alternative Credit Sources for a Fuller Financial Picture

While Equifax, Experian, and TransUnion hold prominence in the credit reporting industry. They are the big three, however, there are other entities that gather and disseminate your private data. Banks, mortgage lenders, and other financial institutions rely on supplementary sources to evaluate your creditworthiness, providing unique perspectives and information not typically found in traditional credit reports.

Comprehending and addressing the insights offered by these alternative credit sources is essential for maintaining an accurate and comprehensive financial profile.

Devoting time to a thorough review and correction of all your personal information is a worthwhile endeavor. Although obtaining additional reports may require some effort, the benefits outweigh the challenges. Credit repair specialists often spend several weeks ensuring their clients’ personal details are accurate across major and minor sources before commencing any dispute procedures. Ultimately this approach saves time, reduces postage expenses, and mitigates frustration.

Overdraft protection plans come with their own set of limits, including how much they cover and how long they last. It’s important to carefully check the specifics of your plan because it might not cover as much as you think.

You can check into alternative option if you are having trouble opening a new account.

- Look for banks or credit unions that don’t rely on ChexSystems or credit reports. GTE Financial’s Go Further Checking, or Varo is an online branch of Bankcorp Bank

- Another approach is to start with a savings account at a small or medium-sized local bank or credit union. Demonstrating responsible savings habits can pave the way for eventually opening a checking account, especially if you consistently increase your savings balance over time.

Fundamental rules:

- Never spend more than you have.

- Avoid dangerously low balances.

- Maintain a cushion of funds in your checking account as a safety net, separate from your regular balance.

This buffer, can be $100 or more, serves as a precaution against overdrafts, fees, and the inconvenience of bounced checks. If tracking your balance is challenging, error on the side of caution and maintain a higher cushion.

The use of personal checks has decreased significantly with the rise of digital payment methods like online banking, and mobile payment apps. Checks remain useful in certain situations where digital payments might not be an option, such as paying rent, settling debts between individuals who prefer not to use cash, or making payments where electronic transfers are not feasible.

They are also used by some who may not have access to banking technology or prefer a more tangible method of payment. Additionally, checks can serve a role in business transactions, particularly among small businesses or in industries that have longer-standing traditions of using checks.

Navigating the Fine Print: Understanding Your Bank’s Checking Account Rules and Overdraft Policies

In the checking account agreement for banks are all slightly different from the next. But overall, have similar terms and conditions. They are written with the banks interest in mind. Sometimes overdrafts fees happen and confuse the owner of the account about why the fee was applied. So here are some of the terms that are hard to read in those checking account agreements that have been overlooked.

For instance, if you postdate a check, the bank can choose to process the check before the date specified, and if there aren’t enough funds in the account to cover the check at that time, it could result in the account becoming overdrawn. In such cases, the bank might charge an NSF fee for the returned check, and if they choose to cover the check anyway (resulting in an overdraft), they may also apply an overdraft fee. Similarly, banks could endorse checks on your behalf if you forgot to sign the check.

ATM deposits might not always go through immediately and could cause issues like bounced checks. Cashier’s checks or money transfers need more time to process, so it’s best not to assume you can use that money right away. Also, banks have daily cutoff times for making deposits, if you make a deposit after the bank’s daily cutoff time, your money won’t be available as quickly as you assume. It’s good to know when your bank’s cutoff time is.

Overdraft protection plans come with their own set of limits, including how much they cover and how long they last. It’s important to carefully check the specifics of your plan because it might not cover as much as you think.

SageStream LLC

PO Box 503793

San Diego, CA 92150

Phone: 1-888-395-0277

Clarity Services: Unveiling Creditworthiness Beyond Traditional Scores

- Clarity Services specializes in predictive analytics for individuals with below-prime credit. With the claim of being a “crystal ball” for predicting future payment behavior, Clarity possesses the largest subprime database in the industry, comprising over 62 million consumers. While conventional credit bureaus assess risk based on past payment history, Clarity focuses on financial and personal stability to determine creditworthiness. Factors such as residential stability, employment consistency, and credit application behavior are analyzed to gauge stability. Longer job tenures are generally viewed more favorably.

Employment History: Are you frequently changing jobs, possibly due to being terminated or unreliable work history? On the other hand, do you have a stable and consistent employment record over an extended period, ideally at least one year, but preferably longer without any yearly job changes for the past five consecutive years?

Credit Applications: Have you recently submitted a high volume of credit applications? A large number of inquiries, particularly for multiple credit cards, raises red flags. Similarly, have you applied for multiple mortgage loans, possibly across various online platforms? It’s common to shop around with two or three different mortgage lenders to find the best home loan option. In this scenario, multiple hard inquiries within a certain timeframe are typically combined and treated as a single inquiry by the credit scoring models.

Credit Score Impact: During times when preserving your credit score is crucial, this combined inquiry treatment is beneficial. Three separate hard inquiries can significantly impact your credit score. If your current score is on the cusp of dropping or rising into the next credit scoring tier, you want to avoid a decrease. A lower score can lead to a higher interest rate on loans. Let me illustrate with an example…

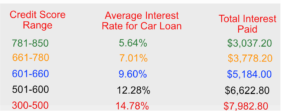

The table shows the interest paid on a $20,000 car loan over 5 years across different credit score ranges, we’ll use the average interest rates provided by Experian for each credit score range. Here’s the breakdown of the average interest rates.

Now, let’s calculate the total interest paid for a $20,000 car loan over 5 years (60 months). The formula to calculate the total interest paid on a loan is:

Where:

- ( P ) is the principal amount ($20,000)

- ( r ) is the monthly interest rate (annual rate divided by 12)

- ( n ) is the total number of payments (60 for a 5-year loan)

Using this formula, we can calculate the total interest paid for each credit score range. Here’s the table with the calculated total interest for each credit score range:

Examine the different credit score tiers and the corresponding total interest amounts. If you have an excellent credit score, say 786, you will pay $3,037 in total interest for that auto loan. When shopping for a car loan, your credit happens to be pulled three times by lenders. Each credit inquiry slightly lowers your credit score. If those inquiries cause your score to drop into the next lower tier, it could result in paying $741 more in total interest on the loan. So, a decrease of just 6 credit score points in this example would cost you an additional $741 in interest charges.

According to Clarity, individuals with prolonged job and address stability, who experienced temporary financial setbacks resulting in late payments, are not perceived as high-risk borrowers. They are seen as trustworthy individuals who endured a temporary hardship. Conversely, frequent changes in residence and excessive credit applications may raise doubts about reliability, as individuals might vanish before fulfilling their payment obligations. If your credit profile is less than perfect, consulting your Clarity Report is advisable.

Clarity Services, Inc.

address: PO Box 5717

Clearwater, FL 33758

Phone: 1-866-390-3118

ChexSystems: The Essential Tool for Uncovering Hidden Financial Histories

ChexSystems is a consumer reporting agency that focuses on tracking debit account history rather than credit accounts. During the process of applying for a mortgage or purchasing a home, lenders may obtain a title report that can reveal information not typically found in credit reports.

This information can include:

- Previous foreclosures or short sales

- Bankruptcies

- Tax liens

- Liens from contractors, service providers, or professionals who performed work on your property and were not fully compensated

- Judgments for unpaid bills, including credit card debt

These negative records are linked to your Social Security number and can persist even if they are not listed on your credit report. It is crucial to disclose any adverse financial events from the past decade openly. A knowledgeable loan officer can verify these details with a title company and provide guidance on the appropriate course of action. Falsifying mortgage applications constitutes felony fraud and should be avoided.

If you have been rejected when trying to open a bank account, it might be due to information in your ChexSystems report. You can obtain your ChexSystems Consumer Report annually for free and request your ChexSystems score, which they provide at no cost. However, this score is different from traditional credit scores and follows a unique scoring system ranging from 100 to 899, with higher scores indicating lower risk to lenders.

To order via mail: Chex Systems, Inc. Attn: Consumer Relations

7805 Hudson Road, Suite 100 Woodbury, MN 55125

To order online: www.chexsystems.com

To order by phone or discuss any concerns: (800) 428-9623

Safeguarding Your Financial Identity: Key Steps to Resolve Disputes and Protect Against Fraud

The most common reason for disputes on Consumer Disclosure Reports is identity theft. This can involve unauthorized activities such as check writing, ATM withdrawals, or even opening a joint account through signature forgery. By the time you notice these activities, the damage is often extensive. If you’re a victim of identity theft, your initial step should be filing a police report.

Another significant cause of negative ChexSystems Reports is merged identities, which occurs when another individual’s banking data is erroneously associated with yours due to similar names. It is crucial to review your Consumer Disclosure Report for accuracy in your name, address, date of birth, and social security number. If you find any discrepancies, submit a copy of your ID along with an explanatory letter and request for correction.

It is important to note that any communication with ChexSystems must be truthful and accurate. If you’ve had a check returned due to insufficient funds, contact the bank where the issue occurred and inquire about a “pay for delete” arrangement. Where they may agree to remove the incident from your ChexSystems consumer report upon settlement of the outstanding balance. Do not deny it because banks are not legally obligated to grant this request. But many will agree if approached politely and directed to the right person.

Another significant cause of negative Chex Reports is merged identities, occurring when another individual’s banking data is erroneously associated with yours due to similar names. Review your Consumer Disclosure Report for accuracy in name, address, date of birth, and social security number. If discrepancies exist, submit a copy of your ID along with an explanatory letter and correction request.

Reset Your Financial Future: Overcoming Credit Challenges and Embracing New Banking Opportunities

Negative information on a Consumer Disclosure Report has the life span of five years. Your credit report is seven years for most negative items. You don’t to wait the full duration before opening a new checking account and moving forward financially.

Mistakes are part of life’s lessons; it’s better to learn from them rather than resent them. Some individuals, open accounts without grasping basic financial management principles. The next thing you know issues begin popping up like unchecked spending and account mismanagement. then worry sets in.

Stress levels rise, it’s terrible. You can take the opportunity to acknowledge past errors and commit to making positive changes moving forward. Today is a new day to begin building a better financial track record.

You can check into alternative option if you are having trouble opening a new account.

- Look for banks or credit unions that don’t rely on ChexSystems or credit reports. GTE Financial’s Go Further Checking, or Varo is an online branch of Bankcorp Bank

- Another approach is to start with a savings account at a small or medium-sized local bank or credit union. Demonstrating responsible savings habits can pave the way for eventually opening a checking account, especially if you consistently increase your savings balance over time.

Fundamental rules:

- Never spend more than you have.

- Avoid dangerously low balances.

- Maintain a cushion of funds in your checking account as a safety net, separate from your regular balance.

This buffer, can be $100 or more, serves as a precaution against overdrafts, fees, and the inconvenience of bounced checks. If tracking your balance is challenging, error on the side of caution and maintain a higher cushion.

The use of personal checks has decreased significantly with the rise of digital payment methods like online banking, and mobile payment apps. Checks remain useful in certain situations where digital payments might not be an option, such as paying rent, settling debts between individuals who prefer not to use cash, or making payments where electronic transfers are not feasible.

They are also used by some who may not have access to banking technology or prefer a more tangible method of payment. Additionally, checks can serve a role in business transactions, particularly among small businesses or in industries that have longer-standing traditions of using checks.

Navigating the Fine Print: Understanding Your Bank’s Checking Account Rules and Overdraft Policies

In the checking account agreement for banks are all slightly different from the next. But overall, have similar terms and conditions. They are written with the banks interest in mind. Sometimes overdrafts fees happen and confuse the owner of the account about why the fee was applied. So here are some of the terms that are hard to read in those checking account agreements that have been overlooked.

For instance, if you postdate a check, the bank can choose to process the check before the date specified, and if there aren’t enough funds in the account to cover the check at that time, it could result in the account becoming overdrawn. In such cases, the bank might charge an NSF fee for the returned check, and if they choose to cover the check anyway (resulting in an overdraft), they may also apply an overdraft fee. Similarly, banks could endorse checks on your behalf if you forgot to sign the check.

ATM deposits might not always go through immediately and could cause issues like bounced checks. Cashier’s checks or money transfers need more time to process, so it’s best not to assume you can use that money right away. Also, banks have daily cutoff times for making deposits, if you make a deposit after the bank’s daily cutoff time, your money won’t be available as quickly as you assume. It’s good to know when your bank’s cutoff time is.

Overdraft protection plans come with their own set of limits, including how much they cover and how long they last. It’s important to carefully check the specifics of your plan because it might not cover as much as you think.

Below are four additional credit report sources worth considering:

- Innovis is the fourth-largest credit bureau, closely trailing Equifax, Experian, and TransUnion. It specializes in data collection, particularly in the bankruptcy domain. Notably, major mortgage entities like Fannie Mae and Freddie Mac share home loan data with Innovis.

Innovis

950 Threadneedle Street, Suite 200

Houston, TX 77079-2937

Phone: 1-800-540-2505 and 1-614-223-0690

- LexisNexis is not a credit bureau. They function as a data service provider, gathering comprehensive information on individuals and supplying it to creditors for risk assessment. It’s a significant source for details on unpaid taxes, judgments, liens, and bankruptcies. Mortgage lenders often utilize LexisNexis to cross-check data not included in traditional credit reports.

LexisNexis

Consumer Center PO Box 105108

Atlanta, CA 30348

Phone: 1-888-497-0011

- SageStream is a legitimate credit bureau. It mirrors the data found on LexisNexis, making it crucial to review both reports for consistency and accuracy. SageStream is utilized by various industries, including automobile lenders, utility companies, cell phone services, retail stores, and credit card companies. Therefore, ensuring the accuracy of all reported information about you, including your name spelling, is crucial. Unlike other scoring systems like FICO or Vantage scores, SageStream employs its own credit scoring system, ranging from 001 to 999. This unique scoring system diverges from traditional methods, possibly to differentiate itself and avoid confusion with other credit scores.

SageStream LLC

PO Box 503793

San Diego, CA 92150

Phone: 1-888-395-0277

Clarity Services: Unveiling Creditworthiness Beyond Traditional Scores

- Clarity Services specializes in predictive analytics for individuals with below-prime credit. With the claim of being a “crystal ball” for predicting future payment behavior, Clarity possesses the largest subprime database in the industry, comprising over 62 million consumers. While conventional credit bureaus assess risk based on past payment history, Clarity focuses on financial and personal stability to determine creditworthiness. Factors such as residential stability, employment consistency, and credit application behavior are analyzed to gauge stability. Longer job tenures are generally viewed more favorably.

Employment History: Are you frequently changing jobs, possibly due to being terminated or unreliable work history? On the other hand, do you have a stable and consistent employment record over an extended period, ideally at least one year, but preferably longer without any yearly job changes for the past five consecutive years?

Credit Applications: Have you recently submitted a high volume of credit applications? A large number of inquiries, particularly for multiple credit cards, raises red flags. Similarly, have you applied for multiple mortgage loans, possibly across various online platforms? It’s common to shop around with two or three different mortgage lenders to find the best home loan option. In this scenario, multiple hard inquiries within a certain timeframe are typically combined and treated as a single inquiry by the credit scoring models.

Credit Score Impact: During times when preserving your credit score is crucial, this combined inquiry treatment is beneficial. Three separate hard inquiries can significantly impact your credit score. If your current score is on the cusp of dropping or rising into the next credit scoring tier, you want to avoid a decrease. A lower score can lead to a higher interest rate on loans. Let me illustrate with an example…

The table shows the interest paid on a $20,000 car loan over 5 years across different credit score ranges, we’ll use the average interest rates provided by Experian for each credit score range. Here’s the breakdown of the average interest rates.

Now, let’s calculate the total interest paid for a $20,000 car loan over 5 years (60 months). The formula to calculate the total interest paid on a loan is:

Where:

- ( P ) is the principal amount ($20,000)

- ( r ) is the monthly interest rate (annual rate divided by 12)

- ( n ) is the total number of payments (60 for a 5-year loan)

Using this formula, we can calculate the total interest paid for each credit score range. Here’s the table with the calculated total interest for each credit score range:

Examine the different credit score tiers and the corresponding total interest amounts. If you have an excellent credit score, say 786, you will pay $3,037 in total interest for that auto loan. When shopping for a car loan, your credit happens to be pulled three times by lenders. Each credit inquiry slightly lowers your credit score. If those inquiries cause your score to drop into the next lower tier, it could result in paying $741 more in total interest on the loan. So, a decrease of just 6 credit score points in this example would cost you an additional $741 in interest charges.

According to Clarity, individuals with prolonged job and address stability, who experienced temporary financial setbacks resulting in late payments, are not perceived as high-risk borrowers. They are seen as trustworthy individuals who endured a temporary hardship. Conversely, frequent changes in residence and excessive credit applications may raise doubts about reliability, as individuals might vanish before fulfilling their payment obligations. If your credit profile is less than perfect, consulting your Clarity Report is advisable.

Clarity Services, Inc.

address: PO Box 5717

Clearwater, FL 33758

Phone: 1-866-390-3118

ChexSystems: The Essential Tool for Uncovering Hidden Financial Histories

ChexSystems is a consumer reporting agency that focuses on tracking debit account history rather than credit accounts. During the process of applying for a mortgage or purchasing a home, lenders may obtain a title report that can reveal information not typically found in credit reports.

This information can include:

- Previous foreclosures or short sales

- Bankruptcies

- Tax liens

- Liens from contractors, service providers, or professionals who performed work on your property and were not fully compensated

- Judgments for unpaid bills, including credit card debt

These negative records are linked to your Social Security number and can persist even if they are not listed on your credit report. It is crucial to disclose any adverse financial events from the past decade openly. A knowledgeable loan officer can verify these details with a title company and provide guidance on the appropriate course of action. Falsifying mortgage applications constitutes felony fraud and should be avoided.

If you have been rejected when trying to open a bank account, it might be due to information in your ChexSystems report. You can obtain your ChexSystems Consumer Report annually for free and request your ChexSystems score, which they provide at no cost. However, this score is different from traditional credit scores and follows a unique scoring system ranging from 100 to 899, with higher scores indicating lower risk to lenders.

To order via mail: Chex Systems, Inc. Attn: Consumer Relations

7805 Hudson Road, Suite 100 Woodbury, MN 55125

To order online: www.chexsystems.com

To order by phone or discuss any concerns: (800) 428-9623

Safeguarding Your Financial Identity: Key Steps to Resolve Disputes and Protect Against Fraud

The most common reason for disputes on Consumer Disclosure Reports is identity theft. This can involve unauthorized activities such as check writing, ATM withdrawals, or even opening a joint account through signature forgery. By the time you notice these activities, the damage is often extensive. If you’re a victim of identity theft, your initial step should be filing a police report.

Another significant cause of negative ChexSystems Reports is merged identities, which occurs when another individual’s banking data is erroneously associated with yours due to similar names. It is crucial to review your Consumer Disclosure Report for accuracy in your name, address, date of birth, and social security number. If you find any discrepancies, submit a copy of your ID along with an explanatory letter and request for correction.

It is important to note that any communication with ChexSystems must be truthful and accurate. If you’ve had a check returned due to insufficient funds, contact the bank where the issue occurred and inquire about a “pay for delete” arrangement. Where they may agree to remove the incident from your ChexSystems consumer report upon settlement of the outstanding balance. Do not deny it because banks are not legally obligated to grant this request. But many will agree if approached politely and directed to the right person.

Another significant cause of negative Chex Reports is merged identities, occurring when another individual’s banking data is erroneously associated with yours due to similar names. Review your Consumer Disclosure Report for accuracy in name, address, date of birth, and social security number. If discrepancies exist, submit a copy of your ID along with an explanatory letter and correction request.

Reset Your Financial Future: Overcoming Credit Challenges and Embracing New Banking Opportunities

Negative information on a Consumer Disclosure Report has the life span of five years. Your credit report is seven years for most negative items. You don’t to wait the full duration before opening a new checking account and moving forward financially.

Mistakes are part of life’s lessons; it’s better to learn from them rather than resent them. Some individuals, open accounts without grasping basic financial management principles. The next thing you know issues begin popping up like unchecked spending and account mismanagement. then worry sets in.

Stress levels rise, it’s terrible. You can take the opportunity to acknowledge past errors and commit to making positive changes moving forward. Today is a new day to begin building a better financial track record.

You can check into alternative option if you are having trouble opening a new account.

- Look for banks or credit unions that don’t rely on ChexSystems or credit reports. GTE Financial’s Go Further Checking, or Varo is an online branch of Bankcorp Bank

- Another approach is to start with a savings account at a small or medium-sized local bank or credit union. Demonstrating responsible savings habits can pave the way for eventually opening a checking account, especially if you consistently increase your savings balance over time.

Fundamental rules:

- Never spend more than you have.

- Avoid dangerously low balances.

- Maintain a cushion of funds in your checking account as a safety net, separate from your regular balance.

This buffer, can be $100 or more, serves as a precaution against overdrafts, fees, and the inconvenience of bounced checks. If tracking your balance is challenging, error on the side of caution and maintain a higher cushion.

The use of personal checks has decreased significantly with the rise of digital payment methods like online banking, and mobile payment apps. Checks remain useful in certain situations where digital payments might not be an option, such as paying rent, settling debts between individuals who prefer not to use cash, or making payments where electronic transfers are not feasible.

They are also used by some who may not have access to banking technology or prefer a more tangible method of payment. Additionally, checks can serve a role in business transactions, particularly among small businesses or in industries that have longer-standing traditions of using checks.

Navigating the Fine Print: Understanding Your Bank’s Checking Account Rules and Overdraft Policies

In the checking account agreement for banks are all slightly different from the next. But overall, have similar terms and conditions. They are written with the banks interest in mind. Sometimes overdrafts fees happen and confuse the owner of the account about why the fee was applied. So here are some of the terms that are hard to read in those checking account agreements that have been overlooked.

For instance, if you postdate a check, the bank can choose to process the check before the date specified, and if there aren’t enough funds in the account to cover the check at that time, it could result in the account becoming overdrawn. In such cases, the bank might charge an NSF fee for the returned check, and if they choose to cover the check anyway (resulting in an overdraft), they may also apply an overdraft fee. Similarly, banks could endorse checks on your behalf if you forgot to sign the check.

ATM deposits might not always go through immediately and could cause issues like bounced checks. Cashier’s checks or money transfers need more time to process, so it’s best not to assume you can use that money right away. Also, banks have daily cutoff times for making deposits, if you make a deposit after the bank’s daily cutoff time, your money won’t be available as quickly as you assume. It’s good to know when your bank’s cutoff time is.

Overdraft protection plans come with their own set of limits, including how much they cover and how long they last. It’s important to carefully check the specifics of your plan because it might not cover as much as you think.