How Long Does It Take To Build Credit From Nothing

The majority of the links on our website are affiliate links. This means that if you click on the link and make a purchase, we earn a small commission at no additional cost to you.

A credit card is generally more practical and beneficial to begin building credit with. Because credit cards offer flexibility, helps build a credit history efficiently, and allows you to manage smaller amounts of debt. However, they are considered the riskiest of credit types. The interest rates are high to start with because of the risk.

A credit account that has been opened for 6 months, used a least once in those 6 months, the account is not in dispute for accuracy will receive a credit score when the credit file is pulled.

Someone who barely ever uses credit, pays the balance in full, on time when they do use it. Depending on how many trade lines they have, within a year they will have a good credit score. Three trade lines that have been paid as agreed on time and maintains a low usage ratio for one year will have an excellent credit score. It takes only one month to blow it. One late payment will drastically drop your credit score. Building credit is ongoing, positive credit events have little impact to credit files. That is why it takes time to build. Negative credit events severely impact credit files. One late payment has the potential of losing 60-110 points from a credit score.

There is not a set number of points a negative event will lose. It depends on how the rest of the credit file looks. High credit scores will lose more points than lower credit scores. A high credit score reflects a long history of responsible credit behavior, including timely payments, low credit utilization, and a balanced mix of credit accounts. The credit scoring models assume that any negative behavior increases the risk of the borrower. But someone with low credit scores already reflects risk. So since higher credit scores indicate great credit behavior, they are penalized more for out of the norm negative events. However, getting back on track with timely payments will not take as long to recover.

You also do not want to have too much credit because it becomes difficult to maintain good credit behavior. Timely payments, low credit utilization, and a balanced mix of credit accounts is what demonstrates that.

Lenders want to see this type of behavior done with a mix of credit types. 10% of your credit score considers the types of credit being used.

Three accounts that includes 2 credit cards and an auto loan will earn more points than three credit card accounts.

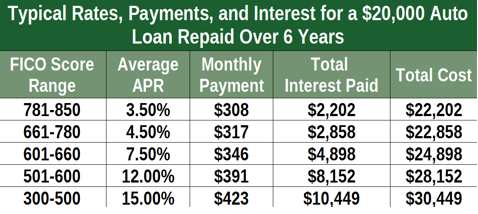

The perfect mix of credit is three credit cards, installment loan, and a mortgage. The three credit cards and installment loan in good standing will give you a credit score that will earn you the best home loans. To get an idea of the difference of cost for great credit scores and low credit scores. But there’s more than the credit score. The score is the result of the credit report.

The Credit Report

A credit report has 5 types of information about a consumer:

- Personal identification data– Name, date of birth, social security number, addresses and phone numbers. You want to have only one form of your name listed on your credit report. With the least number of addresses. In terms of credit scoring, having more than one variation of your name will affect your score suggesting instability. Lenders start to think if the consumer is trying to hide from something because of aliases. The most common form is first name, middle initial, and last name.

- Tradelines– These are your accounts like credit cards you have open, student loans, and home loans. This section is the bulk of information influencing your credit score. It is the consumers track record.

- Collections– If you have any account that has been sold to a collection company, this section will show that. The creditor cannot collect or accept money for the debt anymore, but you still owe the debt. When a charge-off turns into a collection, your score could take a hit twice.

- Public records- This section is reserved for bankruptcies and foreclosures. This section also impacts a credit score negatively. Tax liens and judgements used to show under the public records section.

- Inquiries –Requests made by a lender, creditor, or another party to review your credit report.

Types of credit lines

Understanding the different types of credit can help you make more informed financial decisions and choose the right type of credit for your needs.

These are the 3 main types of credit. There are other types but overlap with the 3 main types.

Revolving credit: (e.g., Credit Cards – Visa, Mastercard) You have a credit limit, and you can use up to that limit. You make payments based on the amount you’ve used, and as you pay off your balance, you can borrow again.

Installment credit: (e.g., Auto Loans, Student Loans) you borrow a fixed amount and make regular payments until it’s paid off.

Open Credit: (e.g., Utilities, Charge cards) These are lines of credit where the balance must be paid in full each month. The balance depends on what you use. If you are late, you are charged late fees, and the account is reported to the credit bureaus as late.

So above you see the credit scoring range. You may notice there are different ranges of scores. Always go by the FICO scoring range because it is the standard for consumer credit. The mortgage industry uses a different FICO scoring model. FICO scores are amazingly accurate in determining risk in individuals paying back what they borrow. That’s what it’s all about “risk”. What’s the risk for lenders? They are giving an individual the ability to make purchases with their money, as long as they pay it back. If they can’t pay it back in full, then there will be interest added to the balance. The lower the score, the greater the risk. Higher interest rates compensate for the increased risk.

Credit scores go up and down all the time. Whenever information is added or deleted from your credit file your score will change. However, your score is not calculated daily. The only time it is calculated is when it is pulled. Whatever is in your file at that time will be scored automatically by the computerized mathematical system. If you made a purchase yesterday and tomorrow your file is going to be updated by the credit bureaus. If you were going to apply for a loan, today would be the primetime to apply. Your credit score is going to be higher today, than it is going to be tomorrow. Because the purchase is going to increase the credit utilization. As it goes up, your score goes down.

If the drop puts you into a lower tier of credit score ranges a monthly payment can be a significant difference.

Influencing Factors in Credit Scoring

The there are 5 factors that make up your credit score. But within the factors there are 40 components that add or subtract points from your score. Here are the 5 factors that affect your score:

Payment history- The most influential factor. Consistency with on time payments is going to influence a strong credit score.

Debt load- The amount of credit that has been used divided by the credit limit gives you a percentage. As the percentage increases, the less points you earn. At 30% you begin losing points. The higher it goes more points will be deducted.

The length of credit- How long has your account been open. The longer you have an open account that has perfect payment history the stronger it is. When an account is closed, it stops earning longevity points. And you lose the credit limit for the account. This increases your debt load. You do not want to close an account, and you definitely do not want the lender to close the account due to inactivity. Use your credit cards at least twice every three months to keep your account active.

Types of credit- Lenders want to see that an individual can manage different types of credit.

Inquiries- There are two types of Inquiries, soft and hard. Soft Inquiries is when creditors do a check on their customers. This helps to reduce risk for the lenders. If a they see a customer has begun making late payments with their other accounts, the lender assumes their going to be next. They can take action by reducing the credit limit and letting the customer know that the interest rate has increased. A soft inquiry doesn’t hurt your credit score. On the other hand, a hard inquiry is when consumer submits an application for a credit line. Hard inquiries deduct points and will remain on your credit report for 2 years. But they only impact a credit file for the first year.

Additional Information

If you are shopping around for the best home loan, you are going to see more than one lender or mortgage broker. The same goes for auto financing, you want the best terms you can get. For these situations you will have a timeframe to shop around, and the credit pulls will count as one inquiry. However, that doesn’t apply for applications for revolving credit (credit cards). If you apply for multiple credit cards within a short period, a lot of points will be deducted because the risk of taking on more credit that can be handled, increases.

Statistics have shown that someone who has six or more hard inquires in the past year is 8 times more likely to declare bankruptcy than someone that has no hard inquires in the past year.

As you can probably tell, the algorithm that’s used in calculating credit scores is very complex. Forget about your credit score and focus on paying the balance in full, on time every month and keep your balances under 10%. You will have an excellent credit score anytime your credit is pulled.