Mastering Credit Scores for Empowered Financial Decisions

The majority of the links on our website are affiliate links. This means that if you click on the link and make a purchase, we earn a small commission at no additional cost to you.

Ordering Your Credit Report

1

Annual Credit Report Request Service

P.O. Box 105281

Atlanta, GA. 30348- 5281

Click here to Download the sample letter for Ordering your reports

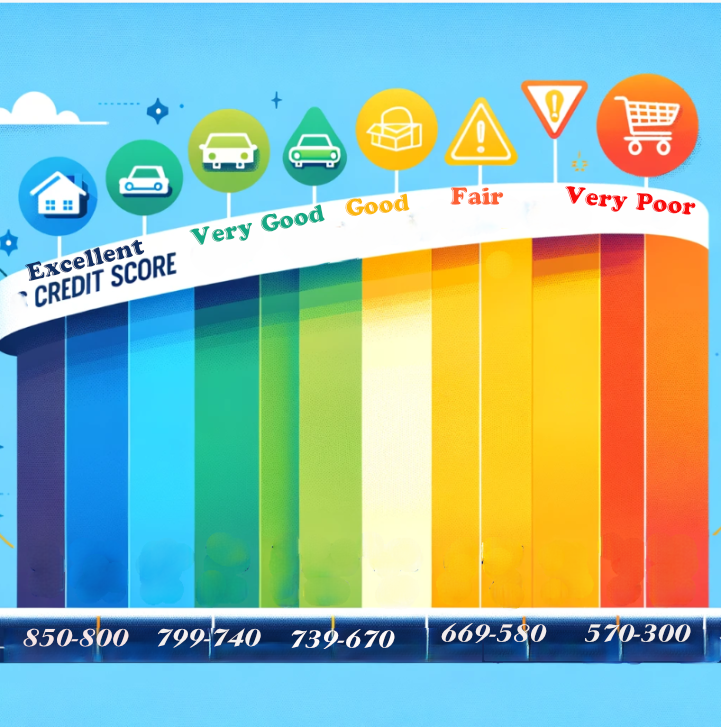

3 digits will indicate whether or not a consumer will be responsible and fulfill financial obligations. Can you handle credit or is it too overwhelming? This number is based on all the information that is found in your credit profile. Your credit profile changes all the time. Data is added and removed from your profile all the time. This results with a different number. The number can be from 300 to 850. The higher the number, the less of a risk you are. Within this range, there are 5 tiers.

- 800-850 Excellent

- 740-799 Very Good

- 670-739 Good

- 580-669 Fair

- 300-579 Very Poor

When Your Credit Score Really Matters

Your credit score is important to know in several key situations where your financial health and capability are assessed by others. Here are some of the main circumstances when knowing your credit score is particularly crucial:

- Applying for a Loan or Mortgage: Lenders will check your credit score to determine your eligibility for a loan and the interest rates you will be offered. A higher score generally means more favorable loan terms.

- Credit Card Applications: When you apply for a new credit card, issuers will look at your credit score to decide whether to approve your application and to set the terms of your credit, such as your limit and interest rate.

- Renting a property: Many landlords use credit scores to assess potential tenants’ reliability. A higher score might improve your chances of securing a rental and could reduce the requirement for a larger security deposit.

- Employment Screening: Some employers check credit scores as part of the background check process, especially for positions that involve financial responsibilities or handling money.

- Insurance Premiums: Insurers may use what’s called a credit-based insurance score to determine your premiums for auto and homeowners’ insurance. A better score can lead to lower premiums.

- Planning Financial Goals: Knowing your credit score can help you understand your financial standing and guide you in improving your financial health, which is beneficial for long-term planning like buying a house or saving for retirement.

- Before a Major Purchase: Checking your score before making large purchases or undergoing significant financial transactions can give you a better sense of what financial products you might qualify for and help you negotiate better terms.

Do not get hung up on your credit score. Your credit score doesn’t exist until your credit is pulled. The FICO’s scoring model will analyze the data in your credit file at that point in time and calculates your credit score. Unless you’re shopping for a home loan or an auto loan, your credit score is similar to a one-time use.

Sometime in the following month your file will be updated. If your credit score is pulled, it will automatically be calculated. It will be a different score.

It’s assumed that credit reports are 100% correct. A lender will not review your credit report with you to make sure everything is correct when you apply for a loan. Your current creditors do not check to make sure there are no overlooked errors in your file when they update it before they report to the credit bureaus.

Evidence shows that the majority of credit reports contain all types of errors. But you’ll never have anyone inform you of errors. Who would even know if your date of birth is wrong on one of your reports? The agency that reviews credit reports and verifies every piece of information on consumer reports is 100% accurate, does not exist. But yet the law states inaccurate information cannot be added to a consumer’s credit file.

The Hidden Errors: Credit Report Inaccuracies

Here are statistics from a study that was conducted by the National Association of State Public Interest Research Groups.

- 79% of credit reports contain errors.

- 54% include personal information that is incorrect.

- 22% of reports have loans that were listed twice.

- 8% of reports were missing positive credit information that boosts credit scores.

- 30% of reports included open accounts that had been closed and paid off. But this can help you if it is a closed account that has been paid-as-agreed. If the closed account has late payments, then it will work against you.

Where is the law at in these situations? Well, the law is waiting for the consumer to request action. Until then, the credit bureaus are not required to do anything. Nothing happens unless a consumer exercises their rights. Unfortunately, consumers are not the credit bureaus customers. We are customers of the furnishers. The furnishers are the credit bureaus customers.

The credit bureaus are just taking the information reported to them and updated the credit files. So, the fault is put on the furnishers. Now the credit bureaus are in the position of taking sides. Do they side with the consumers? Or do they side with their customers?

They are going with whatever their customer says. That is very important,

Practical Tips for Credit Management

If you do these three things,

- keep your overall balance below 10% when all credit cards combined and individually keep card balances under 10%.

- Pay on time.

- pay off balance when it is due, eliminating the possibility of having a balance roll over to the next month.

You will never have to worry about your credit score. You will know that your score is top notch.

Your job is to review your reports. Every three months request one of the three reports you get for free. Making sure your file has not merged with someone else’s file. You’re also checking for possible identity theft. Making sure all your accounts are accounts that you opened. Keep vigilant about identity theft.

Step 1

The first thing you want to do if you have reports from the credit bureaus that are not more than a year old, review them for any inaccuracies. Otherwise you need to order them. This time you want all three reports. After you clean your report, and you know your credit file is 100% accurate. The following years you can order 1 free report every three months to remain vigilant.

If you didn’t know, reporting information to the credit bureaus is voluntary. So, your three reports may not be the same across the board. Maybe one of your creditors only reports to TransUnion. Your other reports will not have that specific account on them. The credit bureaus are just businesses who collect, store, make available, and sell information about consumer’s creditworthiness. The furnishers who report to the credit bureaus pay them to report. The furnishers are then able to use their databases of consumers and they can then market their financial products to targeted consumers.

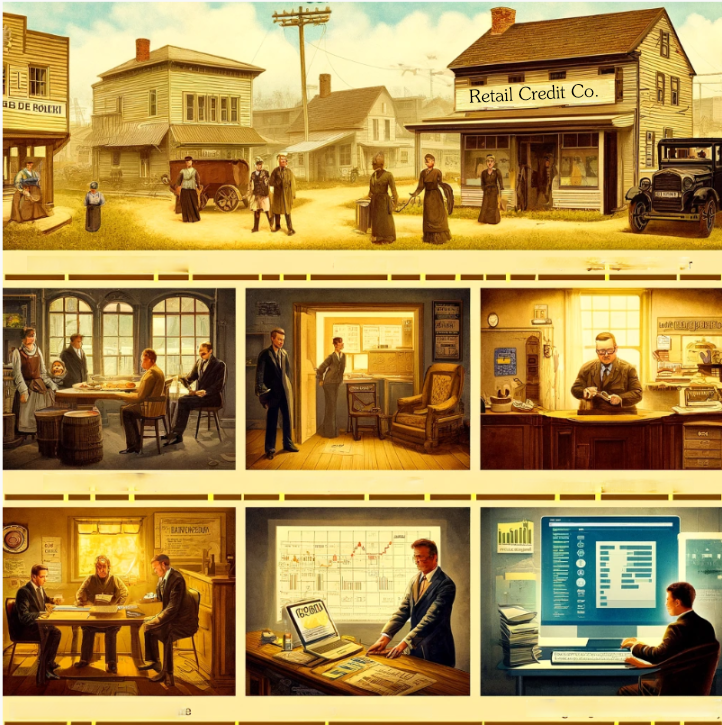

Quick overview of the credit bureaus origins

In the retail sector back in the 1800’s small agencies that were local to their area, started collecting information on the creditworthiness of customers and then selling it. That’s when the idea of collecting information about individual’s creditworthiness was formed. In 1899, the Retail Credit Company began collecting and selling customer credit information to businesses.

In 1975, the company became Equifax. TransUnion popped up in 1968, And Experian was a firm that started in 1960 over in the U.K., who expanded their offices to the United States.

Computer technology in the 1960’s and 1970’s allowed credit files to transition into the way credit information is handled today. The FCRA was passed in 1970 because there was an increase of concern with consumer’s about the privacy and accuracy of this data. It is 2024, 55 years later and we still have privacy and accuracy issues.

Back to step 1 in repairing your credit. Request your credit report directly from the credit bureaus through the mail. Before you can dispute any information with a credit bureau, you need to have your official credit report, as it serves as the basis for your challenges. Reports obtained from loan officers or other 3rd party websites won’t cut it; they are the middleman, and you cannot be sure that the information is the same as the credit bureaus.

The free scores these sites provide are not FICO scores. In the credit and mortgage industries, FICO scores are the standard. You can now purchase your consumer FICO score from FICO. Credit scores that are not FICO scores are only good for using as a gauge for your upward progress for credit repair. Such as VantageScore 3.0 and credit monitoring service websites. Do not rely on them because you will set yourself up for a big disappointment.

Use the address below and send a letter to get your credit reports.

Annual Credit Report Request Service

P.O. Box 105281

Atlanta, GA. 30348- 5281

Click here to Download the sample letter for Ordering your reports

This is important, when you send your request for your report, include a large, clear and clean photocopy of your state ID or driver’s license and a document that verifies your name and address such as a utility bill.

ID Types

- Driver’s license

- Utility bill

- Bank statement

- State ID

- Voter registration card

- Personal voided check.

- Paycheck stub

- Mortgage statement

- Passport

- Rent agreement.

You do this for 2 reasons:

- To prevent identity theft and fraud.

- The bureaus have claimed that some consumers do not send proper identification. Or they cannot read the address on ID’s. They are just stalling, making it harder for consumers.

It is also important that you use a standard #10 business envelope with a first-class mail stamp. This letter can be sent without being certified. Future letters will, but not this one The reason being, certified mail provides you with:

- A paper trail of your dispute process if the need for it comes around.

- Someone needs to sign for the letter. The credit bureaus process millions of credit information every month, it would be too easy for them to say they never received it.

- It works as a timestamp starting their 30-day timeframe to open a dispute, investigate, and respond to your request. If they fail to meet the time limit, the error has to be deleted even if they verify the information as accurate.

Do not order your reports by phone because it’s too easy for anyone to call and request your reports. And receive your information by impersonating you.

And never use the online dispute system. Why?

Behind the Scenes: The Credit Dispute Process

Most people generally expect that an “investigation” into a credit card or loan dispute would include activities such as examining documents, investigating facts, talking to witnesses, or comparing handwriting signatures.

Online dispute system was not designed with consumer’s interest in mind. It’s meant to eliminate as many disputes as fast as possible. E-OSCAR (Online Solution for Complete and Accurate Reporting) is a highly automated, computer-based system that essentially bypasses any thorough investigation.

This system simplifies detailed dispute letters to a two- or three-digit codes, occasionally accompanied by a short narrative. The credit reporting industry communicates disputes to data furnishers using a standardized form called Automated Consumer Dispute Verification (ACDV) form. The credit bureaus initiate investigations with furnishers by sending an ACDV.

An ACDV typically includes a few key pieces: the consumer’s identifying information from the credit bureau’s records, the code that summarizes the consumer’s dispute, and occasionally, a brief narrative of one line that adds context to the code. Some of those code options are

- Not his/hers

- Disputes present/previous Account Status/History

- Claims Inaccurate Information. Did not provide specific dispute

- Disputes amounts

Credit bureau employee selects an appropriate dispute code from a list of twenty-six available options from a dropdown menu.

The code is transmitted to the furnisher without any of the supporting documentation that the consumer provided—documents like account applications, billing statements, letters, and payoff statements that could provide substantial, even decisive, evidence. This omission of crucial documents from the investigation process could potentially breach the Fair Credit Reporting Act (FCRA). But, this is the way it is. You need to work with it because it is not going to change.

After allegedly conducting an investigation, the credit bureaus send out generic and vague letters claiming that an investigation has been completed. These letters lack any specifics about whom they contacted or what information was gathered and used to reach a final decision. Once you request that information, the credit bureau is required to provide it for you.

Furnishers just check a box to confirm that the disputed information has been verified. Often, furnishers are just verifying the existence of disputed information, instead of actually investigating the dispute. They will not actually research the underlying dispute, review documents, or speak to consumers about the dispute. Instead, these furnishers simply confirm that the information in the ACDV matches their computer records, and then verify the disputed information to the credit bureaus.

Now you know what goes on behind the curtain. I cannot guarantee success with these steps because even with laws set in place, no one really knows what the credit bureaus will do. But you can follow what successful credit repair experts do to get results.

Credit Repair Company: The Horrible Truth

The credit repair business seems to be a perfect avenue for the inexperienced and the scammers who just want your money. Because there is one major aspect that a consumer cannot control. What the credit bureaus will do? Laws are ignored, loopholes are used.

Which is why nobody can guarantee results. They can only guarantee a credit repair business can give is to do their best and will not give up. The perfect excuse for the inexperienced and scammers. They charge you an arm and a leg, and at the end when they don’t come through and then you now have to pay for the expensive service that you feel swindled from. While they claim they did their best and they didn’t give up after sending 3 rounds of letters. Results cannot be guaranteed.

The Credit Repair Organizations Act

The Credit Repair Organizations Act is the law that protects the consumer from the bad guys. Here is an overview:

-

Prohibited Practices: CROA outlines specific practices that credit repair organizations are forbidden from engaging in. For example, these organizations cannot make false or misleading statements about their services, such as guaranteeing to “erase bad credit” or to completely remove accurate negative information from a consumer’s credit report.

-

Disclosure Requirements: Credit repair organizations are required to provide a written contract to consumers that outlines the services to be performed, the payment terms, and a detailed timeline for when the services will be provided. Consumers also have the right to cancel this contract within three days without any penalty or obligation.

-

False Claims: Organizations are barred from making any false claims about their abilities to improve a consumer’s credit score, and they cannot create a “new” identity legally for a consumer by using a different social security number or other federal identification.

-

Litigation: Consumers have the right to sue credit repair organizations for violations of the CROA. If successful, they may be entitled to recover damages, attorney’s fees, and costs.

- Payment Structure: The act prohibits these organizations from charging or receiving any payment until the promised services have been fully performed. This provision is designed to protect consumers from paying for services that do not meet the promised outcomes.

Some individuals may not have the time or patience to work on improving their credit. But might have the financial resources to hire a professional. Thankfully, there are reputable companies available that can effectively handle the job. However, it’s important to be careful and ensure that you don’t end up wasting your money. You should be wary of credit repair companies that outsource their services or yield minimal results even after working on your credit for over a year, leading to prolonged and unproductive efforts.

Number 5, payment structure above regulates credit repair companies from receiving payment until the promised services are complete. Credit Saint has a good track record, but they ignored number 5 because there is an initial working fee. I have noticed quite a few credit repair companies have this junk fee.

Many people from other industries decide to get into credit repair such as Loan officers, former schoolteachers and Entrepeneur’s. You need to be careful if you decide to go down this road. Here is a scenario for you; I call a credit repair company and ask how many years’ experience their credit repair expert has.

They tell me 8 years’ experience. What they don’t tell me is that the credit repair company is a franchise. The franchise has successfully been around, operating for 8 years. And the “expert” really has 7 years’ experience reviewing credit reports as an underwriter. And only 18 months real-world hands-on credit repair experience.

If you are going to hire a credit repair company, make sure they have at least 5 years hand on experience. You’ll need to do some research. Such as checking for any posted complaints for the company over at www.ripoffreport.com.

Search for complaints by doing a Google search on the company, also search for the company on Yelp.com

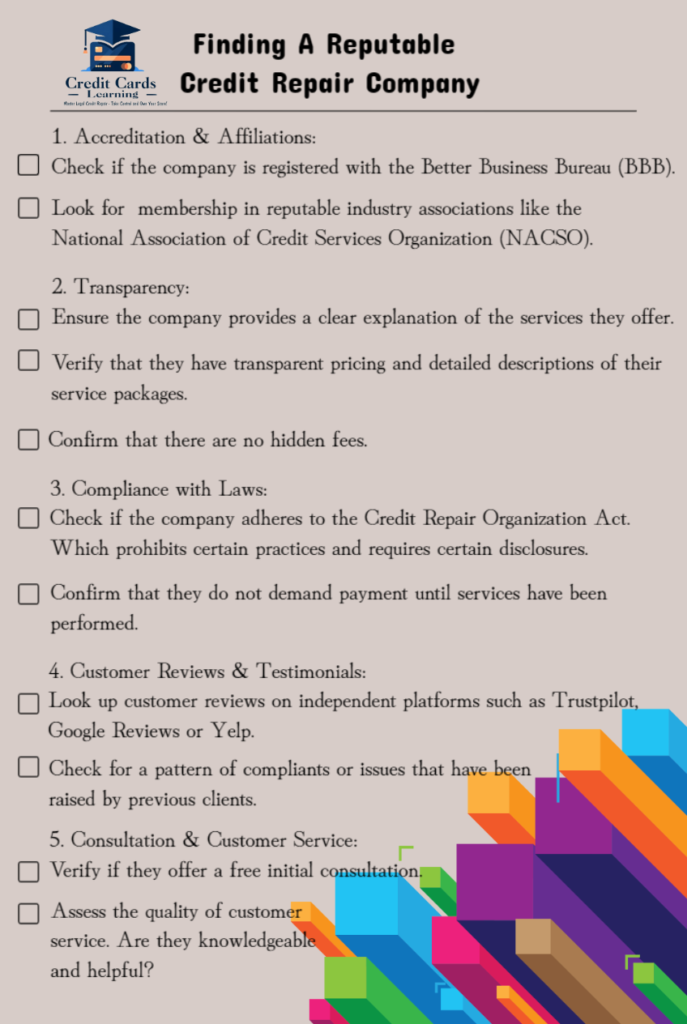

Checklist For Finding A Reputable Credit Repair Company