We may earn money or products from the companies mentioned in this post.

A poor credit file is a file with many late payments, usage on credit cards is close to their limits. Whereas a thin credit file is one with less than 3 tradelines. A credit history consisting of one credit card is notably thin. Lenders want to see that you can manage your money and use credit responsibly. Your credit score tells the lender if you’re a good or bad financial risk. Your credit report is your track record, backing it up.

Debit card usage does not show on credit reports. Nor do they help build credit. Keep in mind that it typically takes six months for a newly opened revolving account to positively impact your credit score when making timely payments. However, negative activity will show almost immediately.

Does that make sense? Hopefully you’ve begun to establish your credit profile. Let’s explore how the credit scoring system operates. Being well-informed puts you in control of the situation. Here’s the thing, Equifax, Experian, and TransUnion do not maintain ongoing scores. They are not saved. Instead, your credit score is calculated in real-time. Your credit file sits on a server. No one at the credit bureaus review your file. When your credit report is pulled, at that very moment the lender’s calculating software calculates a score based on the information on file at that moment. All the information used to calculate the score, is printed out as your report.

Credit scoring is a complex equation. But this is the question: What is the difference between great credit and horrible credit?

Answer:

- 1.) Pay on time.

- 2.) Keep a low balance-to-limit ratio. (If your balance is over 50% of your credit limit, you will lose points even when making on time payments.

- 3.) Pay the entire balance off when the bill statement arrives.

Let’s continue, the credit bureaus only know what is reported to them. They do not investigate, that’s a key point to know. Their credit investigators are really data entry clerks. If they were allowed to investigate, they wouldn’t know what to do or where to start. They are not qualified to perform investigations. Then again, their definition of an credit investigation is not the same definition the rest of the world knows. The credit bureaus just collect and sell consumer information. I used to think that they were a government agency, Nope, they are just a business, data collectors. There are laws that the credit bureaus have to follow, but there is no law that makes reporting information to them mandatory, it is 100% voluntary. But yet they have more influence over consumers’ lives than any other company. Because the majority of financial dealings depend on the credit scoring system.

The scoring system is software that was introduced in 1956 by Fair, Isaac, and Company. Ever since then they have been the standard. Majority of lenders use FICO’s scoring model. The mortgage industry uses FICO’s scoring model. Furthermore, lenders use a more relaxed scoring model than the mortgage industry. But they are both FICO scoring models. The purpose of Fair, Isaac, and Company software is to give lenders an index of risk.

By analyzing all the information on a credit file. It is amazingly accurate most of the time. The credit bureaus are competitors but the 3 joined forces and created VantageScore. They’re trying to push their scoring system onto the mortgage industry. For the time being, FICO is what the mortgage industry uses. So, VantageScore mean nothing. Only about 10% of lenders use VantageScore. At first, they used a range of 501 to 990. Consumers were confused so VantageScore switched to 300 to 850 to match FICO’s range. Their credit score range is the same as FICO’s, but the algorithms are not. They could not figure out what FICO’s scoring algorithms are. The same goes for credit monitoring and credit score websites. They tried to figure out the algorithms of FICO, but they can’t figure it out. And FICO is not sharing their scoring models with anyone.

If you want your FICO score for free, (myFICO.com/free) this is NOT an affiliate link.

Keep in mind that your real credit score is the credit score you receive when you’re applying for a loan to purchase a house. I mentioned above that FICO has many different scoring models. The mortgage industry uses a version that only mortgage broker’s use. Once you choose who your mortgage broker will be, they will tell you your score and show you your report. Do not let any lender pull your credit when you are shopping for a mortgage. It’s good practice. The credit bureaus sell trigger leads. When mortgage companies pull credit reports. The credit bureaus take note, then sell consumer’s information to competing mortgage companies who will pay to know who is actively searching for mortgages.

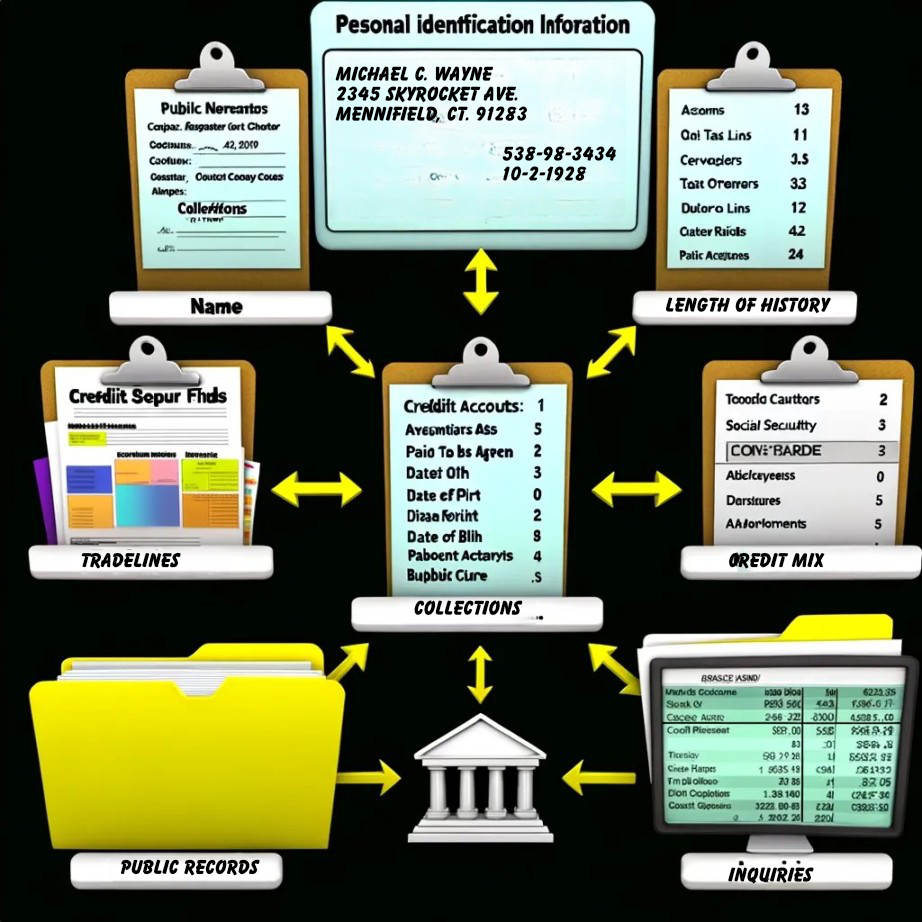

What Information Is on Your Credit Report

- Personal Identification Information This includes your name, any variations of your name you’ve used, addresses where you’ve lived, date of birth, social security number, and current and past employers.

- Trade Lines These are accounts you currently have or have had in the past seven years. Details provided include the creditor’s name, account number, the highest balance, current balance, and payment history. Payment statuses include “paid as agreed,” 30 days late, 60 days late, and 90-plus days late. Additionally, the report includes the date the account was opened, the closing date if the account is closed, and the Date of Last Activity, which is significant for credit scoring purposes.

- Collections This segment details accounts that are significantly overdue and have been transferred to an external collection agency. If an account is overdue but handled by the collection department of the original creditor, it is still listed under trade lines (this does not improve your score).

- Public Records This section includes information on liens such as tax liens, judgments, and bankruptcies, as well as foreclosures (where a mortgage lender reclaims a home due to non-payment). These are termed public records because they are accessible to anyone who visits a courthouse. Credit bureaus employ a third party to collect this information from public records and report it to them. This is the only type of information for which they pay.

- Inquiries This part lists the creditors who have requested your credit report.

How is Your Score Calculated?

- 35% of your credit score is determined by your payment history. This includes whether you paid your obligations on time as agreed or if there were any delays. Negative credit events like collections, bankruptcy, and foreclosure also fall into this category and can result in the largest point deductions.

- 30% of your credit score is influenced by your debt ratio. Specifically, for credit cards, it examines your balance-to-limit ratio. Utilizing a small portion of your available credit positively affects your score, while being maxed out can negatively impact it. It’s important to note that this only applies to revolving credit, not to installment loans; therefore, having a high balance on your student loan won’t harm your score. Revolving credit refers to accounts that do not have a fixed number of payments, such as those with a Visa card.

- 15% of your credit score depends on the length of your credit history. The age of your accounts matters; a long-standing history of timely payments is beneficial. Achieving a credit score of 800 requires time.

- 10% of your score is determined by the variety of credit types you manage. Holding a mortgage can significantly boost your score. Installment loans, like student loans or auto loans, also positively contribute. Credit cards have a smaller impact. Ideally, having a diverse mix of credit types is beneficial for the consumer. Do not take out loans from payday loans or finance with a finance company because they are hard money lenders. It doesn’t matter if you pay the loan off in time, they will negatively affect your score.

- 10% of your credit score is influenced by inquiries. Why is this significant? If you have multiple inquiries from different credit card companies in a short period, it could suggest that you’re preparing to take on substantial debt. This raises concerns about your capacity to meet existing financial obligations. On the other hand, multiple inquiries from different mortgage lenders or auto finance companies are typically seen as rate shopping for a single house or vehicle, not as intentions to acquire multiple properties or vehicles simultaneously.

There are two types of credit inquiries. One type doesn’t affect your credit score at all, while the other type does impact your score.

Soft Inquiries

A soft inquiry occurs when a credit card company checks your credit report to verify if there have been any recent late payments. This review is performed automatically by computer software that scans millions of credit files. For instance, they might target everyone in certain zip codes who have a credit score above 720 and send them credit card offers. There is just not enough time for them to have an individual do this manually.

Your current credit card and mortgage companies will review your credit report for any late payments to safeguard their interests. If they notice you were late with a payment on your Discover card. Visa might increase your interest rate, even if you’ve always been punctual with them. This is 100% legal as long as they inform you in fine print. They do this under the assumption that you might start falling behind on payments with them as well, viewing you as a high-risk borrower and significantly raise your interest rate to a steep level, such as 32%.

Although, your mortgage company’s loan note prevents them to increase your interest rate based on late credit card payments due to the fixed terms you have agreed upon. But if they do see your falling behind on your financial commitments, they may contact you to offer a refinancing option to consolidate your credit card debt. Often, this isn’t in your best interest, as it involves taking on a larger loan that consumes more of your home equity.

On a Side Note

Consumer Credit Counseling and similar debt management organizations make a situation worse. Creditors often report to credit bureaus that the account is under the management of a debt relief agency. Did you know all lenders look at this as being in a Chapter 13 bankruptcy? Because an account that is in a debt management program shows a lender that the individual is unable to manage their finances on their own. That is the complete opposite of what a lender is looking for.

To top it off, as long as the consumer is in the debt management program making on-time payments, the creditor is reporting the account as being late on payments. Because they have not paid-as-agreed. The agency negotiates a lower payment. This breaks the original agreement with the lender. However, it is possible to secure an FHA loan while enrolled in a Consumer Credit Counseling Service if you meet three specific criteria:

- You have been adhering to the payment plan for a year or more.

- You have made all payments to creditors on time.

- You have received written permission from the CCC Service to apply for a mortgage.

Hard Inquiries

If you’ve ever clicked on an internet advertisement for a mortgage, take note. These ads can be misleading. They might lure you with a simple prompt like, “Find out what rates are in your area,” enticing you to enter your zip code—seemingly harmless at first. However, this leads to more probing questions, and before you know it, you’re providing highly personal details like your social security number, and of course, your email address to receive further information.

Buried within this process is often fine print authorizing them to access your credit report. The need for your social security number is typically for this purpose: to conduct a hard credit inquiry. Unlike a soft inquiry, a hard inquiry occurs when you apply for credit—whether it’s for a credit card, auto loan, mortgage, or personal loan—and the lender checks your credit report with your permission.

Such inquiries will lower your credit score. Statistics indicate that individuals with six or more inquiries in the past year are eight times more likely to file for bankruptcy than those with no inquiries. This underscores why not to let a lot of lenders pull your credit report and why you should not apply for a mortgage quote online from lead generators like Lending Tree who sells your private information to multiple lenders.

Removing Hard Inquiries

If a company pulled your credit without your permission, you have the right to have that inquiry removed from your report. By insisting on verification or validation of the inquiry. Request comprehensive details such as the date consent was given, the method of obtaining consent, the name of the individual who authorized and conducted the credit check and documented proof of consent. If these details can’t be provided, or the provider doesn’t want to provide them, you have the right to have the inquiry removed. Remember, unauthorized credit pulls are illegal.

Sample Letter for Deleting Hard Inquiries

Impact of Inquiries on Your Credit Score

Many individuals are concerned about how inquiries might affect their credit reports and their ability to secure favorable mortgage rates. Inquiries contribute the least to credit scores, making up only about 10%. For the majority, this minimal impact is negligible. However, for those with borderline credit scores—scores that are close to transitioning to a higher or lower category—it’s an important consideration. Here are the FICO credit score ranges, where marginal scores are those on the cusp of entering a new range.

Credit Score Ranges

- 800-850 Excellent

- 740-799 Very Good

- 670-739 Good

- 580-669 Fair

- 300-579 Very Poor

Multiple credit card inquiries can negatively affect your credit score. This is because it’s quite possible to acquire several credit cards simultaneously, significantly increasing your debt and consequently your credit risk.

The impact on your credit score from negative events, like late payments, varies depending on your credit history and there isn’t a fixed number of points that will be deducted. The more time that has elapsed since a negative event, the lesser its impact on your score. For example, a recent 30-day late payment will harm your score more than a bankruptcy that occurred several years ago. This is because, from the credit bureaus’ perspective, an old bankruptcy is considered resolved, while a new late payment might indicate the beginning of financial troubles.

Tips for a Stellar Score

To attain the highest possible score in the shortest duration, here are some of the best practices. Even if they appear challenging, it’s essential to persevere, as you’re cultivating new, beneficial habits that will ultimately help you achieve your financial goals.

Over time, a challenging habit transitions into a routine, then eventually becomes effortless. Like the old saying goes, practice makes perfect. – while initially demanding, with consistency, it becomes more manageable.

- Ensure your balance remains extremely low by refraining from charging more than 29% of the permitted limit. For instance, if your limit is $300, aim to keep the balance below $87, or even lower if possible. Make small purchases, like five dollars, and promptly pay them off upon receiving the bill. Borrowing less associates with better scores. However, it’s essential to use your credit card occasionally to demonstrate responsible credit usage; thus, strive for an “ultra-low” balance rather than completely abstaining from usage.

- Ensure to settle the entire balance in full upon the bill’s arrival. Points will be deducted if you opt for paying the minimum or any amount that carries over part of the balance to the following month. Maintaining a balance does not showcase responsible credit usage. Carrying a balance indicates exceeding your budget and exhibiting poor credit management.

- Utilize more than just one credit card. Solely relying on your preferred rewards card while neglecting others could hinder your efforts to build a strong credit score. Demonstrating responsible management of multiple accounts is key, while ensuring you keep a low balance.

- Here’s a useful tip for homeowners: it’s advisable to refrain from obtaining a Home Equity Line of Credit (HELOC) shortly before seeking additional financing. This is because a new HELOC can temporarily decrease your credit score.

- Regularly utilize each of your credit cards to prevent their closure by the issuer. If a line of credit remains inactive for an extended period, the lender may terminate the account without prior notification. Because if they do not generate revenue from merchant fees or an annual fee, maintaining the open account has no benefit for them. As a result, if your account is terminated, your credit score could decline for two primary reasons. Firstly, the overall available credit limit is diminished, and secondly, the duration of your credit history may be shortened. The duration considered as “a long time” varies depending on the institution. Typically, major credit cards may cancel accounts after 12 to 24 months of inactivity, while store cards often have longer grace periods. It’s easy to overlook a card that isn’t frequently used, and by the time you receive a notification letter regarding its cancellation, it may already be too late to take any corrective action.

Let me give you an example, I have visa, discover, and a Citi cards. The limit on my visa is $1,000. My discover has a limit of $1000. And Citi has a limit of $1000. My overall available credit is $3,000. I just added the limits for each card together for my overall available credit. The three credit cards also get scored individually. This is why credit utilization is important.

Now, I have used $500 on visa and Discover. My Citi card has a $0 balance. I’m utilizing $1000 of the $3000 available. My credit utilization is 33%. I just divided 1 by 3. I will lose points because I am over 30%. Individually, Discover and Visa are both 50% utilized. I will lose points for both cards. I will earn points for my Citi card because there is no balance on it.

Now let’s say Citi card was closed due to inactivity. I will lose the individual points on the card. And I lost $1000 available credit. Now my overall available credit is $2000 and I’m still utilizing $1000 but now my credit utilization is at 50%. When it was at 33%, I lost points, but now that it’s at 50%, my score is going drop a significant amount.

That is the one way a closed account is going to hurt my rating. The second is length of history. Let’s say I had Citi for 3 years. Let’s also say that I was earning 60 points everytime my score is calculated for that one account. If it remains open the account is going to get older and giving more points. But it closed so I still get 60 points for it, but eventually the account will be gone from my reports and if it is a good standing account it’s going to hurt when it is gone.

Strategic Credit Score Boosts

If you were going to apply for a car loan. And you wanted to raise your score, you can ask your creditor to increase the limit. This will raise your overall available credit, at the same time lower the credit utilization. Remember borrowing less associates with better scores.

Now that you know what information is on your credit reports, when your score is calculated and how your score is calculated. You can take all that information and use it to your advantage. For instance, if you significantly reduce your credit card balance, you’re going to earn a lot of points.

However, creditors typically update your payment history monthly. If you make a payment on May 18 and the creditor reports on May 20, but your credit report is pulled on May 19, it won’t reflect this most recent payment and lower balance, so you won’t see the score improvement you earned. Knowing this allows you to strategically time when to authorize a credit check.

Ideally, you’ll maintain a low balance and these strategic boosts won’t even matter. Since reporting dates vary by creditor, you can contact your creditor to find out their specific reporting date, especially if it’s crucial for your plans.