How to Effectively Dispute an Inaccurate Debt on Your Credit Report

The majority of the links on our website are affiliate links. This means that if you click on the link and make a purchase, we earn a small commission at no additional cost to you.

5

If you are at this point, the inaccurate information you want deleted from your file is being validated. You may have received a letter stating: “Unfortunately, we are unable to remove the disputed information reported on your credit report. To preserve the integrity of the credit reporting system, we are unable to alter or remove valid information reported to the credit reporting agencies.”

What is your next move?

Well, you will now send a letter requesting written proof no matter who you are sending your letter to. But there are different letters that depend on who you are sending the letter to.

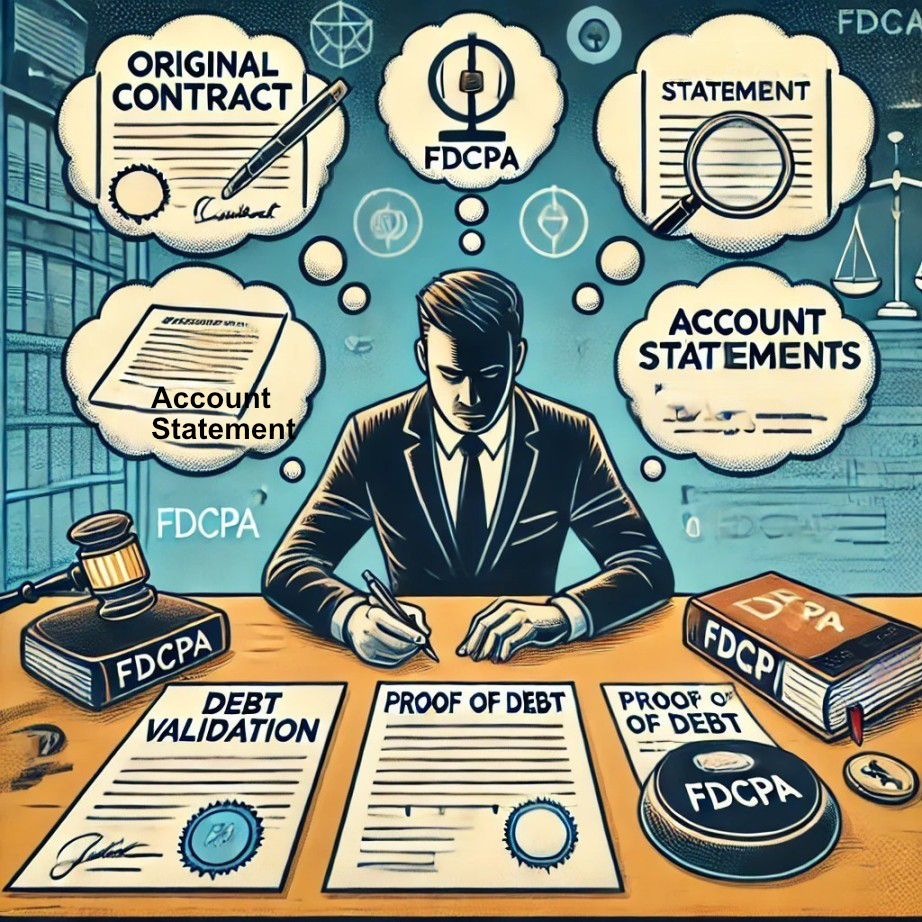

The terms “debt validation” and “proof of debt” are related but apply in different contexts and have distinct requirements.

Debt Validation

Debt validation applies specifically to debt collectors and is governed by the Fair Debt Collection Practices Act (FDCPA). When a debt collector contacts a consumer about a debt, the consumer has the right to request validation of the debt. The debt collector must provide the following:

- Verification of the Debt: Information about the amount of the debt and the name of the creditor to whom the debt is owed.

- Evidence of Ownership: Proof that the debt collector has the legal right to collect the debt, which typically involves a transfer of the debt from the original creditor to the debt collector.

- Details of the Debt: A statement providing details of the original debt, including the original creditor’s name and the amount owed.

The consumer must request this validation in writing within 30 days of being contacted by the debt collector. The debt collector is required to stop all collection activities until the debt is validated.

Proof of Debt

Proof of debt applies to creditors, the original entities that provided the credit or loan. Creditors must provide evidence that the debt is valid and that they have the right to collect it. This typically includes:

- Original Contract or Agreement: A copy of the original agreement or contract that established the debt, showing the debtor’s signature.

- Account Statements: Detailed statements showing the transactions, charges, payments, and balance history.

- Proof of Ownership: Documentation proving that the creditor owns the debt.

Key Differences

Applicability:

- Debt Validation: Applies to debt collectors who are attempting to collect a debt on behalf of another entity.

- Proof of Debt: Applies to creditors, the original lenders or entities that extended the credit.

Legal Basis:

- Debt Validation: Governed by the FDCPA.

- Proof of Debt: It is not governed by any specific act. However, in order for a creditor to establish the legitimacy of the debt, these documents are what will prove legitimacy.

Content of the Request:

- Debt Validation: Focuses on the legitimacy of the debt collector’s right to collect and the basic details of the debt.

- Proof of Debt: Focuses on the complete details and history of the debt, including the original agreement and detailed account statements.

Summary

- Debt Validation: Ensures that the debt collector has the right to collect the debt and that the details they provide are accurate.

- Proof of Debt: Requires the original creditor to provide comprehensive documentation proving that the debt is valid and detailing the debt’s history.

By understanding these differences, you will be able to navigate your rights and obligations when dealing with debt collectors and creditors. When you request debt validation or proof of debt, they are legally bound by that request and cannot ignore it. If any documents are missing, it is not proper validation. You have the right to send a letter to the credit bureau demanding they delete the information.

The Art of Debt Validation: Unveiling Credit Bureau Secrets

The creditor is not allowed to continue reporting the account to the credit bureaus, they cannot collect any money from you, and they are not allowed to contact you about the debt. With debt validation and proof of debt, you are banking on the fact that the creditor doesn’t have one specific document on hand. The original contract that you signed when you opened the account. Maybe they don’t have the time or inclination to locate your original document that has your signature on it because of the inconvenience.

Medical offices keep excellent records. Some creditors do and some do not. If it is a new account, they probably will have no trouble locating the document. However, if the account is established, paper records may be stored offsite, and locating the document will take time.

If you are in good standing with the creditor, it would make more sense to delete the information and keep their customer, you, happy. However, if you are in bad standing with the creditor, they will ensure they provide proof because you have not upheld your end of the agreement. And they are probably not too happy with the situation.

If it is a debt collector, the older the debt the less likely the debt collector is going to have the original credit agreement. Generally, as debts are transferred or sold, maintaining complete and accurate records can become more challenging.

The chances of a debt collector having a copy of the original credit agreement for the debtor can vary depending on several factors including the age of the debt, the policies of the creditor, and the practices of the debt collection agency. Here are a few considerations:

- Age of Debt: Older debts are less likely to have the original credit agreement readily available. As debts are sold and transferred between different collectors, documentation may be lost or not transferred completely.

- Type of Debt: Certain types of debt, like credit card debt, may not involve a detailed “credit agreement” as one might expect with a mortgage or a car loan. Instead, they might be governed by the terms of service agreed upon when the account was opened, which might be updated periodically.

- Creditor Policies: Some creditors maintain thorough records and transfer these to debt collectors when selling the debt. Others may not keep detailed records or may not transfer all documents to the agency.

- Collection Agency Practices: Some debt collectors maintain comprehensive records and can easily access original agreements, while others may not prioritize keeping detailed files.

- Legal Requirements: Depending on the jurisdiction, there may be legal requirements for debt collectors to retain and provide original credit agreements upon request, particularly if the debtor disputes the debt or requests verification.

How to Challenge Credit Bureaus and Win the Credit Repair Game

You know that credit repair is not a one size fits all. Your situation may have a better outcome by sending letters to creditors. I am going to stick to the general steps. So, we are going to send the next letter to the credit bureaus that show the inaccurate information. We have sent them a letter requesting an investigation be done on the matter. Knowing that they do not investigate, and they do not look over any documentation. You have been keeping track of the letters you have sent. So, you know what date you sent a letter and the date in which they received it.

We expected them to verify the information and send you a response letter back. They are stalling. Trying to deflate your balloon. This tactic works well for them. A lot of people would have quit by now. Who can blame them? It’s frustrating .

They are not expecting you to send a letter back. We want to see what happens when you call B.S. on them.

They should have provided you with the specifics of their investigation. But it was not requested and they are not obligated to.

So let’s request to have their method of verification because you do not believe them. Send this letter certified mail, because they are now obligated to provide you with the specifics. If you do not receive the receipt that shows the letter was signed for, they can say they never received your letter. “It was lost in the mail.”

They now know that they need to provide specific information to you. What determined the information to be valid? What documents were reviewed? You want to know the exact steps they took to verify the information. Who was the investigator? You need their name and contact information so you can communicate with them.

The credit bureaus do not what to give written details of their investigation and hand them over to anyone. It is not like the public doesn’t know. But they cannot lie and write a false report. Stating that they spoke to the furnisher and had them pull out their records and reviewed documents. They can’t do that. That would be a lie and in writing.

And they also do not want to write what actually occurred and hand it over to a consumer. But they are required to because you requested it. They do not want to tell you that they outsourced the dispute to the Philippines, nor do they want you calling their agent and the agent saying something they are not supposed to. In fact, the vendor’s do not have phones at their workstations with the disputes that are outsourced.

Their other option is to delete the information altogether, and the problem goes away.

Sample of Method of Verification

Sample Letter for Incomplete Debt Validation